Industry insights

Budget 2025 insight

Executive summary

No stamp duty reform, no demand side incentives and no mention of any reforms to corporation tax incentives, suggesting that all hope for building 1.5 million homes rests squarely with reforms to the planning system. Even the widely anticipated decision not to proceed with proposals for a convergence of the standard and lower rates of landfill tax are quite what it seems due to the cash equivalent RPI uplift applied to the standard rate also applying to the lower rate, resulting in a 115% increase to the lower rate from 1st 2026 and a 470% overall increase in the period to 1st April 2030.

Capital allowances offered little respite with an announcement of a reduction in the main pool plant and machinery writing down allowances from 18% to 14% which is set to cost industry £7bn over the same term. The only bright note being the introduction of a 40% first year allowance for plant and machinery costs for unincorporated businesses and for expenditure that would not otherwise qualify for full expensing.

What the budget said

Landfill tax: the government confirmed that it had listened to industry and will not proceed with the proposed convergence of the lower and higher rates. Instead, they will increase the standard rate of Landfill Tax by RPI and the lower rate by the cash amount of the increase in the standard rate, maintaining the differential between the two rates in cash terms. Allegedly, to avoid imposing unavoidable costs on businesses or undermining the government’s target of building 1.5 million new homes in England. OBR predicted cost to industry: £420m over the period to 2030-31.

Land remediation grant: Funding from the Department for Environment, Food and Rural Affairs (DEFRA) will provide public bodies with grants to remediate land where landfill tax is an unaffordable blocker. This is expected to increase land available for development and other means, and lead to a net increase in remediation-associated landfill tax receipts. There is no data on the value of these grants.

Land remediation relief: there was nothing in the budget either to acknowledge the consultation responses or to introduce any of the reforms to the relief called for by industry including ourselves and the Homes Builders Federation and British Property Federation and many others.

Capital allowances: In a surprise move, the government has deferred tax relief on plant and machinery expenditure by reducing the annual writing down allowance (WDA) on main pool plant and machinery assets from 18% to 14% whilst at the same time introducing a first-year allowance of 40% for plant and machinery expenditure incurred by unincorporated businesses and leased assets and for expenditure that would not otherwise qualify for full expensing. OBR predicted cost to industry: £7bn over the period to 2030-31.

R&D Expenditure Credits: The government will pilot a targeted advance assurance service from spring 2026, enabling small and medium-sized enterprises to gain clarity on key aspects of their R&D tax relief claims before submitting to HMRC. The government is also publishing a summary of responses to the advance clearance consultation.

Impact

So, what does this all mean in practice.

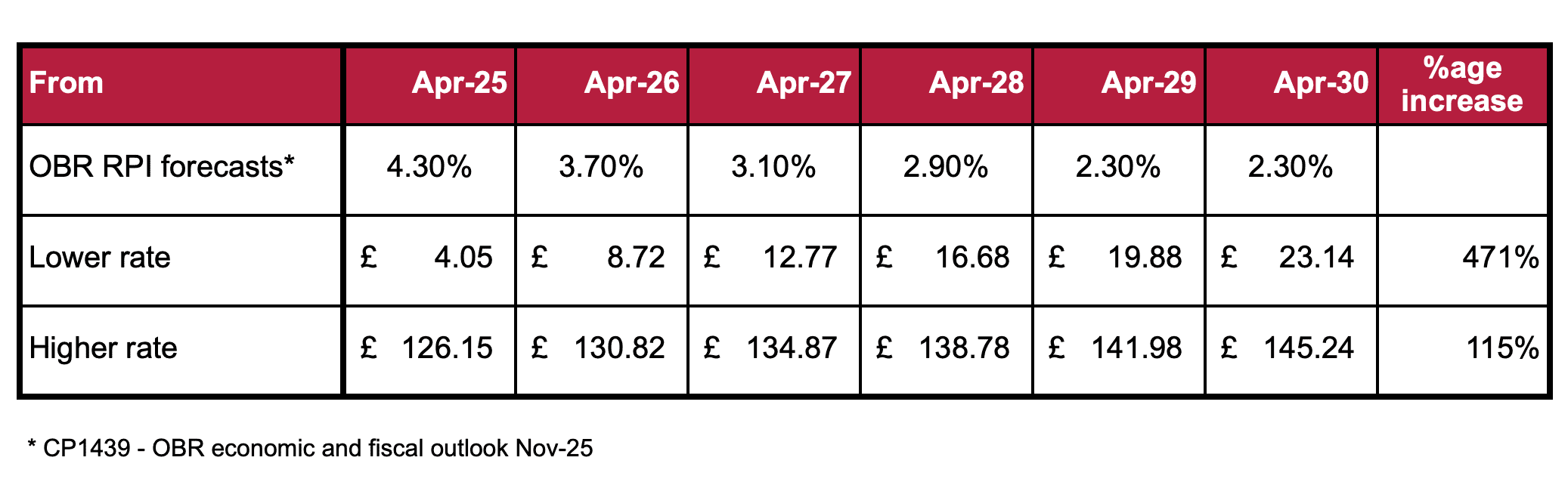

Landfill tax: the landfill tax standard rate will increase by RPI from 1st April 2026 taking the rate from £126.15 a tonne to £130.82 using OBR RPI forecasts, an increase of £4.67 per tonne which will also be applied to the current lower rate of £4.05 per tonne to a new rate of £8.72, representing a massive 115% increase in year 1 and over 470% increase over the term to 2030 based on the OBR RPI forecasts in the table below:

Inner city developments involving large scale basement excavations of clays and soils will be most impacted by this measure and could significantly increase the cost of development in urban areas where there is a heavy and necessary reliance on underground basement structures where land values are high.

Capital allowances – WDAs: from a planning perspective the reduction in the main pool writing down allowance from 18% to 14% will make first year allowances relatively more attractive. Importantly, full expensing, like all first-year allowances, must be claimed in the year the expenditure is incurred. This is particularly relevant on large multi-year developments which extend beyond the general two-year time limit for making a claim. If the first-year allowance is not claimed in the period it becomes due, it will default to the lower 14% WDA rate.

Capital allowances – FYAs: the introduction of the new 40% first year allowance is not replacing the full expensing allowance but is intended to apply for unincorporated businesses who are currently unable to access full expensing. This means income taxpayers acquiring new plant and machinery will be able to access the 40% allowance.

REITS: capital allowances help reduce Property Income Distributions (PIDs) and REITs, like other companies, have the option to claim a first-year allowance or just add the qualifying expenditure to the main pool and claim at the default WDA. PID forecasting is important for investors and so is the creation of a smoothing effect for the allowances generated from new developments and acquisitions. Strategic consideration and use of first year allowances on certain buildings means that it is possible to retain a similar level of allowances to that provided for under the 18% WDA regime.

Land remediation relief: our view is that the HM Treasury team dealing with LRR have not yet had time to consider the consultation responses and will be seeking further market evidence on the impact of potential changes to the relief. So, expect something in the next budget and please come forward with any examples of schemes whose viability relies on the benefits derived from the relief.

Author: Ben de Waal